In 2025, rising health insurance premiums are increasingly pressuring households in Malaysia financially. To cope with the costs, more families and individuals are adjusting, downgrading, or even canceling policies. These trends create vulnerability during medical emergencies and add to stress and uncertainty. This article explores the reasons behind premium hikes, the impact on consumers, and actionable strategies Malaysians can use to maintain affordable coverage while protecting their health.

Why Health Insurance Premiums Are Increasing in Malaysia

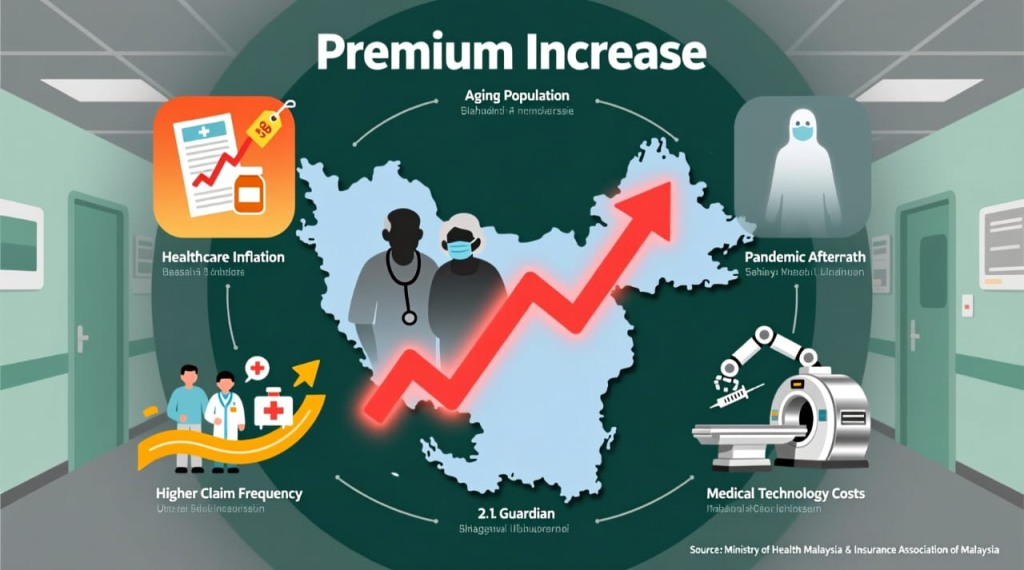

Several key factors have led to the increase in premiums, making health insurance less affordable for many Malaysians.

Healthcare Inflation: The cost of medical treatments is shooting upwards. Most consultations, surgeries, diagnostic tests, and prescriptions bear an increased cost in hospitals, clinics, and pharmacies, respectively. Insurers pass these on to policyholders, leading to increased premiums across the board.

Aging Population: Malaysia’s population is steadily getting older. The more adults over 50 there are who need frequent medical attention, the more frequent the claims will be. Insurers adjust the premium for all policyholders in order to balance out the financial risk.

Long-term Impact of the Pandemic: COVID-19 has had lingering effects on the insurance market. Insurers are still facing increased claims about hospitalizations, treatments, and long-term complications. Insurers were hence forced to adjust the premium rates.

Higher Claim Frequency : More Malaysians are actively using their insurance for routine and specialized medical care. Rising claim frequency forces insurers to increase premiums to maintain financial stability.

Medical Technology Costs: Advancements in medical technology include imaging, robotic surgeries, and new medicines. These improve outcomes but are very costly. Their adoption by hospitals raises operational costs, which insurers then pass on to the policyholder.

These factors, combined, create an increasingly difficult environment where health insurance, particularly for middle- and lower-income households, is becoming increasingly harder to afford.

How Rising Premiums Affect Malaysian Consumers

The increase in premiums extends more than financial decisions, reaching coverage decisions and mental well-being.

Policy Downgrades and Cancellations: A lot of Malaysians are downgrading or canceling their policies in order to reduce monthly expenses. While this provides temporary relief, it leaves them at risk of unexpected medical costs.

Financial Vulnerability: Not being properly covered leads to a lot of out-of-pocket expenses for routine hospital visits, surgeries, and critical illnesses. Even small medical incidents run the risk of blowing into major financial liabilities.

Reduced Benefits: In most cases, downgrading policies loses crucial coverage, such as critical illness protection, comprehensive hospitalization, or specialist consultations. This trade-off leaves households exposed to serious health risks.

Mental and Emotional Stress: The increasing premium and financial uncertainty make families anxious. The apprehension of future medical bills affects the mental well-being of each member, family stability, and productivity at work or school.

Shifting to Public Healthcare: Some Malaysians, particularly younger adults or middle-income families, are shifting to public hospitals to save on costs. This tends to put a strain on the public healthcare resources, resulting in longer waiting times and affecting the quality of care.

Key Statistics and Market Insights

According to reports, policy adjustments and cancellations are on the rise among Malaysians due to premium hikes, although detailed nationwide data remains sketchy.Depending on age, type of coverage, and claim history, average premium increases have ranged from 5% to 10% per year.Younger adults are more likely to cancel coverage because of financial pressures, while older adults keep their policies regardless of the increased cost.

Competition remains tight in the Malaysian health insurance market, with incentives such as wellness rewards and bundling discounts to retain policyholders.BNM has, in some instances, stepped in to prevent highly excessive premium increases and make them more affordable by capping increases and encouraging a multiple-year phasing of adjustments.These insights show that people are becoming increasingly concerned about affordability and the need for strategic planning.

Strategies to Keep Health Insurance Affordable in 2025

Despite rising premiums, Malaysians can employ workable cost-containment methods that do not necessarily undermine essential coverages.

Compare Insurance Plans: Websites like RinggitPlus enable consumers to compare several insurance plans in a very short period of time and thus find those policies that balance coverage and cost effectively.

Increase the Deductibles: Higher deductibles will lower the monthly premiums. Though the out-of-pocket expenses during claims increase, the strategy works for the rare users of medical care.

Bundle Policies: When putting health insurance together with life, motor, or home insurance, substantial discounts are unlocked that reduce overall annual expenditure. Bundling can be an effective method for households seeking multiple coverage options.

Review Coverage Needs: Scrutinise current policies carefully to get rid of unwanted add-ons. Keep the necessary core coverage like hospitalization, critical illness, and routine care to avoid paying for benefits you never use.

Adopt a Healthy Lifestyle : Insurers often give discounts to those policyholders who keep good health through regular exercise, preventive screenings, and wellness programs. In this respect, health-conscious policyholders might enjoy overall lower long-term costs.

Negotiate with insurers: Some insurers offer flexible plans, discounts, or customized coverage. Speaking to insurers directly can unlock savings that may not be apparent in their standard plans.

Government Assistance Programs: The MySalam program offers basic health coverage to low-income Malaysians, which provides a safety net against large medical expenses. Eligible households could lower their financial burden while still having important protection.

These strategies help balance affordability with sufficient coverage, thereby reducing the financial vulnerability of households in case of medical emergencies.

FAQ – Rising Health Insurance Premiums Malaysia 2025

Why are the premiums increasing so fast?

The factors contributing to increasing premiums are medical inflation, increased claim frequency, persistent pandemic-related medical costs, and the adoption of sophisticated medical technologies.

Can I negotiate premiums with insurers?

Flexible plans or discounts exist with some insurers, although availability does vary. Discuss this directly with providers for the best solution.

Are there government programs that may help with coverage?

Yes, MySalam and all other similar initiatives in the country offer basic coverage to all eligible low-income Malaysians, covering major medical costs.

What are the risks of canceling insurance?

Canceling insurance exposes individuals to high out-of-pocket expenses and loss of important benefits, including critical illness and hospitalization coverage.

Can I go to a more affordable plan without losing necessary coverage?

Yes, but with new plans, it’s important to carefully review to make sure the essential benefits remain intact.

Conclusion

Accordingly, ever-rising health insurance premiums in Malaysia are inflicting increased financial burdens in 2025, which is encouraging policy downgrades, cancellations, and heightened stress among households. It therefore involves consumers remaining informed about commercially available policies, making regular comparisons, and using strategies for economizing to retain decent levels of cover. Knowing what drives premium increases, using practical strategies, and availing oneself of available incentives and government programs can help Malaysians protect their health as well as their finances. Proactive planning will ensure that households remain covered during medical emergencies without facing unaffordable costs, even in a market of rising premiums.