Homeownership is still one of the major financial milestones Malaysians strive for, and the affordability of it largely rests on the housing loan interest rates . In 2025, the rates are dependent upon the Overnight Policy Rate, the bank-specific spread, borrower profiles, and the nature of the property. Understanding how rates are built and what influences them helps prospective buyers compare loan options with clarity.

How housing loan interest rates are determined

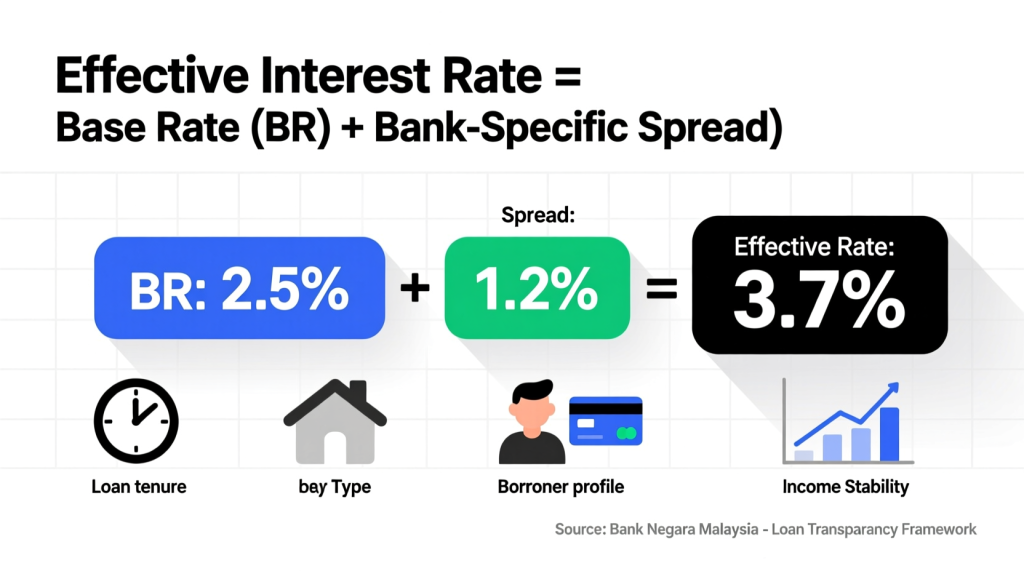

Banks in Malaysia quote home loan rates by adding a bank-specific spread to the BR. This gives the effective annual interest you will pay. For example, a BR of 2.5% plus a spread of 1.2% computes to about 3.7% on a housing loan. Rates vary with the tenure of a loan, the type of property, and the borrower’s credit and income profile. This promotes transparency and makes comparison across banks simple.

Current housing loan rates in 2025

Typically, for the year 2025, Malaysian housing loan rates fall between 3.5% to 4.2%. Here are indicative examples from major banks:

- Maybank : BR 2.5% + 1.2% = ~3.7%

- CIMB Bank: BR 2.45% + 1.25% = ~3.7%

- Public Bank: BR 2.52% + 1.2% = ~3.72%

- RHB Bank : BR 2.6% + 1.3% = ~3.9%

Rates vary based on the shift in OPR and the internal policy of each bank. Your individual profile and ongoing promotions can tilt the final rate.

Key Factors Shaping the Housing Loan Rates

Several factors go into Malaysia’s home loan rate calculations:

Overnight Policy Rate (OPR): BNM’s adjustments affect the BR and, subsequently, the loan rate.

Bank Policies and Spreads: A spread reflecting risk and strategy is set by each bank individually.

Borrower profile: Credit score, income stability, and existing debt matter.

Property type and location: Prime residential properties are usually able to negotiate lower rates than commercial or less desirable ones.

Understanding these components helps borrowers read the rate structures correctly.

Fixed versus floating rates

Borrowers can opt for fixed and floating rate schemes:

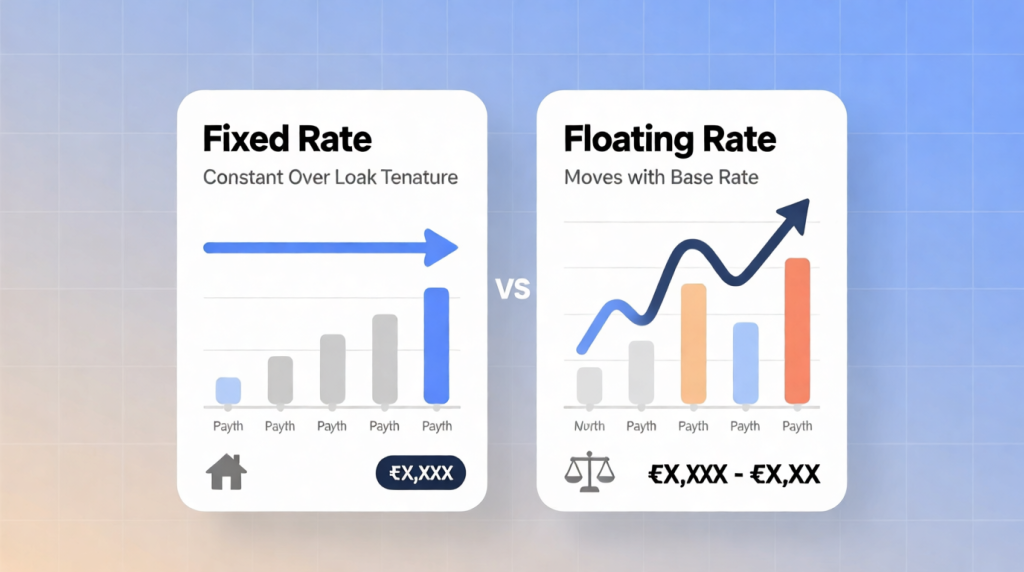

Fixed rates : remain constant over the whole tenure of the loan and provide very predictable monthly repayments. They are usually higher than floating options.

Floating rates: They move with the Base Rate. This means monthly payments would vary. They can sometimes be lower when OPR is stable or falling.

Banks provide a number of packages. Floating rates are the rule in 2025.

2024 vs. 2025 Rate Snapshot

For 2024, housing loan rates remained relatively stable, anchored by an OPR at 3.00%. The standard lending rates typically ranged from 3.9% to 5.2% depending on bank and package.

Bank Negara Malaysia reduced the OPR in July 2025 to 2.75%. This freed up lower effective lending rates as banks rebalanced their base rates and spreads to reflect the policy shift.

2026 outlook

Forecasts for 2026 are cautious. The OPR is projected to stay at 2.75% until at least 2027 unless big changes occur in the economy. This might move with domestic growth, inflation, and global trade conditions. A robust recovery or higher inflation could push up the rates, while steady growth with low inflation may keep them steady.

How to evaluate housing loans

Shop around across banks, test your repayment capacity, and consider tenure options. Longer tenures reduce monthly payments but increase total interest. Shorter tenures increase monthly costs but decrease overall interest. Negotiate spreads based on your credit and income, and compare promotional offers to find the most competitive loan.

Frequently Asked Questions

Q: What is the average housing loan rate in Malaysia for 2025?

A: Generally 3.5% to 4.2%, vary by bank and package.

Q: How does the OPR affect rates?

A: When the OPR changes, banks adjust the Base Rate, which directly moves housing loan rates.

Q: Fixed vs. floating, which is better?

A: Fixed gives stability; floating can save money if rates drop. It depends on your risk tolerance and repayment goals.

Q: Can rates be negotiated?

A: Yes,banks can lower spreads for borrowers with good credit and stable income.

Q: Does property type and location matter?

A: Yes, the prime residential areas normally attract lower rates compared to commercial or less sought-after properties.