Source : https://www.bnm.gov.my/

Bank Negara Malaysia has kept the Overnight Policy Rate at 2.75% for 2025. The move signals a careful, balanced stance: support for growth, guardrails for inflation, and a focus on keeping everyday costs manageable for Malaysians in a year of global uncertainty and choppy markets. The OPR touches many parts of daily life-from home loans and personal borrowings to business financing and overall consumer confidence.

Predictability for both households and businesses is achieved by keeping the OPR steady. With stable borrowing costs, families can plan budgets with more confidence, small firms can access financing without surprise spikes, and investors get reassurance that Malaysia’s financial landscape remains supportive of growth.

Understanding the OPR and its wider ramifications enables Malaysians to make informed decisions in 2025. This article explains what the OPR is, why BNM left it unchanged, and what households and businesses can expect in practical terms.

What is the Overnight Policy Rate?

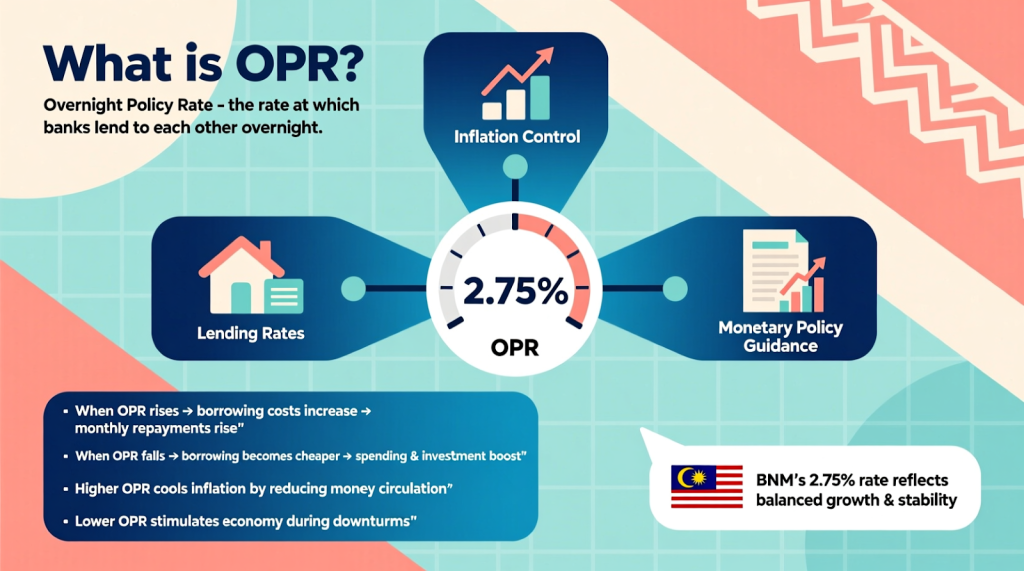

The OPR is described as an overnight interest rate at which banks lend to each other. Although it may sound technical, OPR shapes daily financial life across the breadth and depth of Malaysia. The main roles it plays include influencing lending rates, controlling inflation, and guiding monetary policy.

Influencing Lending Rates: The OPR influences the interest rates that banks charge for mortgages, personal loans, credit cards, and business loans. When the OPR increases, it makes borrowing more expensive; its decrease makes borrowing cheaper. This translates into higher or lower monthly repayments for households and affects investment and expansion decisions for businesses.

Controlling Inflation: Inflation is a general increase in prices of goods and services. Through adjusting the OPR, BNM affects the amount of money circulating in the economy. A higher OPR cools down borrowing and spending, reining in inflation. Similarly, an OPR cut will boost borrowing and spending activities, therefore boosting overall activity during slack periods.

Guiding Monetary Policy: The OPR acts as a tool to stabilize the economy. Such rate decisions are normally taken based on domestic growth, employment, consumer spending, and global trends. Keeping the OPR at 2.75% suggests BNM sees conditions supporting both stability and sustainable growth.

To Malaysians, the understanding of OPR is important because this sets the tone for personal finance, investment choices, and budgeting.

Why Bank Negara Malaysia Held the OPR Steady

Considering the various internal and global factors, BNM had opted to maintain the OPR at 2.75% in 2025:

Moderate Inflation: Malaysia’s CPI indicates that inflation is within the desirable range. Essential commodity prices are increasing within manageable levels, and therefore there isn’t a compelling need to raise borrowing costs to reduce spending. A steady OPR eases the pressure on households that are already battling day-to-day expenses.

Stable economic growth: GDP steadily grows. Recovery from the pandemic is ongoing but not red-hot, so aggressive tightening isn’t warranted. A stable rate supports gradual, sustainable rebound, giving room for businesses and consumers to plan.

Global Financial Uncertainty: International markets continue to be volatile because of geopolitics, external rate adjustments, and supply chain problems. Holding the OPR steady is a cautious move to shield Malaysia from sudden shocks.

Household Borrowing Pressure: Most households in Malaysia have housing loans, education loans, and personal loans. Keeping the OPR steady keeps repayments predictable; this reduces financial stress and enables planning for needs such as healthcare, education, and daily needs.

Overall, the decision signals a clear priority: steady economic footing while protecting households’ financial well-being.

How the OPR Affects Borrowers and Households

The OPR directly influences the cost of borrowing, and therefore budgets and planning.

Mortgage and Loan Payments: Homeowners with loans linked to OPR have more stable monthly payments, which help them make long-term plans in renovation, education, or savings without the fear of a sudden rate hike.

Credit Cards and Personal Loans: Interest on personal borrowings usually follows the OPR. Stable rates improve the predictability of household debt repayments and avoid monthly surprises.

Business financing: SMEs and larger firms use loans for operational needs, equipment, or expansion. Predictable, reasonable loan rates enable businesses to invest more, hire more labor, and plan with more certainty.

Cost of Living: Lower borrowing costs alleviate overall financial stress, freeing up income for essentials, savings, or discretionary spending that helps to keep economic activity moving.

In other words, a stable OPR lets households and businesses plan, invest, and spend with more confidence, supporting financial stability across the nation.

Economic and Market Impact

BNM’s stance also nudges Malaysia’s financial system and economy in several ways:

Bank Lending Behaviour : Banks are likely to maintain lending rates relatively stable across loan products, which would continue to support borrowing and investment.

Investment Confidence: Predictable rates improve investor confidence and attract both local and foreign capital with longer-term commitments.

Currency Stability: A stable OPR would mean ringgit stability against other currencies, which will help importers, exporters, and traders dealing with international markets.

Stock Market Performance: Stable rates tend to buoy equities since steady borrowing costs support consumer spending and business profits.

Overall, the decision balances stimulating domestic activity with keeping inflation and risk in check.

Practical Tips for Households

Take full advantage of a stable OPR by following these practical steps:

Assess loan terms: whether fixed or floating rates suit you best. For floating-rate loans pegged to the OPR, stability aids in planning.

Budget carefully: Arrange monthly expenses, including loan repayments, utilities, groceries, and other expenditures, using predictable borrowing costs as a guideline.

Track Inflation: Inflation is a watch on the price change of essentials, fuel, and utilities. Even with a stable OPR, inflation can still dent overall costs.

Consider Refinancing: If the prevailing terms are more favorable, consider refinancing home or personal loans. A stable OPR creates avenues for favorable terms.

FAQ – Bank Negara OPR 2.75%

1. What does keeping the OPR at 2.75% mean?

This means that the borrowing rates will remain relatively stable, easing the financial burden from households and businesses.

2. Will my mortgage or personal loan rate change?

Rates linked to OPR might stay put; the banks are best spoken to for details.

3. How does the OPR impact the cost of living?

Stable rates help predictable loan repayments, supporting household budgets.

4. Does BNM plan to change the OPR soon?

Any future moves would depend on inflation, growth, and global conditions.

5. How can this be used for financial planning?

Use stability to better plan borrowing, savings, and investments in 2025.

Conclusion

BNM’s move to maintain the OPR at 2.75% reiterates its commitment to steady economic growth with consideration for households’ affordability. To the ordinary Malaysian, it provides clarity in how mortgages, personal loans, and business financing will be managed. Understanding what OPR is and the implications it has will enable households and businesses alike to make appropriate financial decisions that enhance budgeting and long-term security in 2025.